Yes you are reading it right, the street might be excited about the recent talk of Reliance Globalcom deal with Batelco, we at InvestorZclub believe that the expected deal , that could possibly value Reliance Globalcom at around 6500 crores, will be hugely negative for the RCOM shareholders and mathematically stock should come down to levels of Rs 62 post deal conclusion.

Yes you are reading it right, the street might be excited about the recent talk of Reliance Globalcom deal with Batelco, we at InvestorZclub believe that the expected deal , that could possibly value Reliance Globalcom at around 6500 crores, will be hugely negative for the RCOM shareholders and mathematically stock should come down to levels of Rs 62 post deal conclusion.

Here is the math:

------------------

At the end of Q3 FY-13, RCOM had net debt of around 37,500 crores, and the stock was valued at around Rs.70 during Feb 2013 (the month of Q3 result announcement) which valued the equity portion of RCOM at around 14000 crores.

So total enterprise valuation during Feb 2013 was approx: 37500 + 14000 = 51,500 crores

With expected consolidated EBIDTA of 6500 crores for FY-13, the company was valued at around 8 times EV to EBIDTA which was 23% higher than the Airtel's current EV to EBIDTA valuation of 6.5 times.

Now suppose the deal happen and RCOM is able to reduce it debt by 6500 crores to 31,000 crores.

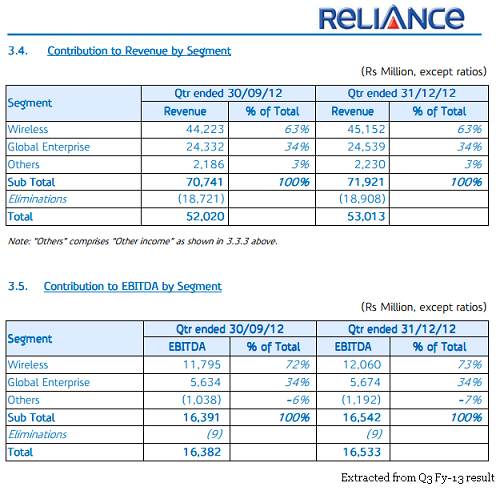

Now as per the given snapshot taken from RCOM Q3 result, the Reliance Global Enterprise had a contribution of 34% to the overall consolidated EBIDTA of RCOM. Though the exact contribution of Reliance Globalcom to RCOM's total EBIDTA is not known explicitly but a rough calculation based on the deal size suggest that it should not be less than 1000 crores. So after deal the overall EBIDTA of RCOM would come down by at least 1000 crores reducing the EBIDTA of RCOM to around 5500 crores.

So post deal if we again value the company at 8 times EV to EBIDTA, the Enterprise valuation for RCOM come to approx: 44000 crores.

With total debt at around 31,000 crores post deal the total equity of the company should be valued at 13,000 crores vs. the current value of 17,700 crores on 19th April 2013.

So mathematically the stock should come down by 27% from the current levels of 85 suggesting a target price of Rs.62.

Reliance Globalcom is a very strong company and has significant contribution to RCOM's consolidated revenue and EBIDTA, and since RCOM has failed twice before in it's attempt to monetize assets, it might have to sell the company at less than potential value.

In long term fundamentally RCOM should not be valued at an EV to EBIDTA valuation of more than 6.5 times, at least at par of Bharti Airtel if not less. If valuation settles at 6.5 times the stock might witness huge downside. Hence at InvestorZclub we feel that people should avoid this stock at all levels.

Now it is being heard that the deal with Batelco is cancelled but a set of new PE players are in to buyout Reliance Globalcom. But the consequence of the deal remain the same. The players have changed. Hence the outlook on stock is still negative..

ReplyDelete